Fur babies booming: Your pets at home have become big business

· Citizen

The global pet care industry is expected to grow by around 6-7% year on year – or materially faster than global GDP growth of roughly 3-5% annually – for years to come.

Visit grenadier.co.za for more information.

As demographic trends shift to ageing populations, with young people marrying and having children later (if at all), the rate of pet adoption in households is steadily rising.

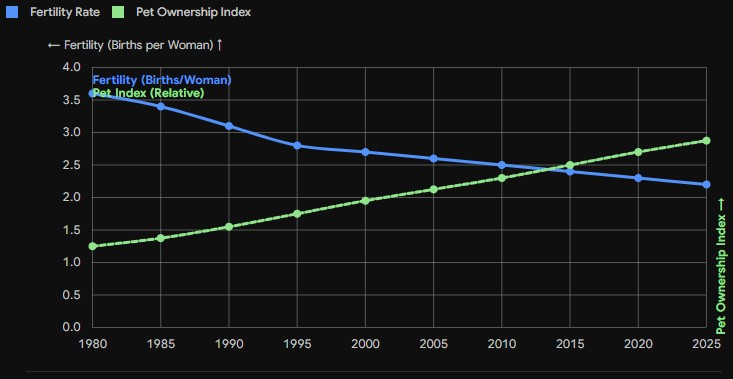

Figure 1 (below, along with the other charts) shows this trend globally and, if you zoom into the faster ageing populations of Asia for example, it can be seen to be accelerating.

Fertility rates versus pet adoption rates (globally and regionally)

{kind=link}

Why do these trends exist, and how are they linked?

Given these demographic changes, people are increasingly viewing their pets as ‘part of the family’ (otherwise known as ‘pet humanisation’). Likewise, decisions for having children later effectively leave vacuums that pets are starting to fill.

Following this elevation of status of these surrogate children or ‘fur babies’, consumer spending on them (much like on human children) is becoming more inelastic with premiumisation aspects as well as growing healthcare aspects.

Together, these trends make pet care a high-growth industry with significant potential.

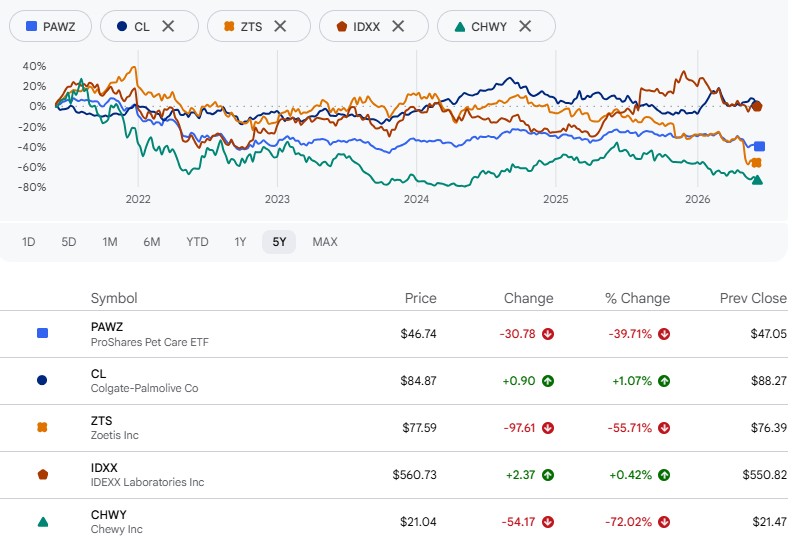

Then why has this segment of the market underperformed the broader market (as represented by ProShares Pet Care ETF or ‘PAWZ’ versus the S&P 500 Index).

ProShares Pet Care ETF relative to S&P 500 Index

{kind=link}

Source: Google Finance (04/06/2026)

The short answer is likely a combination of pet care not attracting the same level of excitement as AI and technology, as well as the sector’s incoming valuations being too high in the first place.

That said, as the pet care market carries on growing, its many constituent parts and listed players share prices keep drifting lower, its valuation becomes more attractive and, eventually, its higher growth rate should lead to higher industry returns.

Other than the passive play that gives you global exposure to the majors here, what other routes into this market are there?

Globally, you could look at the leader in veterinary pharmaceuticals (including both pets and livestock), Zoetis Inc, but its steadily expiring and increasingly commoditised patent portfolio is eating its own growth rate.

Similar and different, Idexx Laboratories offers an entry-point into veterinary diagnostic hardware and software.

Shifting more clearly into the consumer pet space, Chewy Inc is basically the ‘Amazon of the petfood sector’ in the US (except for the fact that Amazon itself now offers pet food deliveries from its marketplace).

In my opinion, the better way to play this market is through globally dominant, higher-end brands, namely Hills, which is owned by Colgate-Palmolive, or those offered by Nestlé.

Colgate-Palmolive is probably the cleanest entry-point into this space, and its Hills brand is perfectly positioned for both the premiumisation and healthcare-driven demand vectors (while the other side of its business, oral care, offers its own wonderful economics).

Thus, it should not be a surprise to consider that Colgate-Palmolive has outperformed both the broader pet care sector and all the other major counters in it.

Colgate-Palmolive and pet care peers

{kind=link}

Source: Google Finance (04/06/2026)

Looking locally, some of our listed retailers have moved decisively into this space, with Woolworths’s acquisition of Absolute Pets and Shoprite’s Petshop Science offering consumers greater choice in pet care retail.

On the manufacturing side, however, there are few pure-play options, with RCL Foods standing out through brands such as Bobtail, Canine Cuisine, Catmor and Feline Cuisine, alongside Sabvest Capital’s investment in Valemount Trading (see its brands here).

Finally, some of the insurers, like OUTsurance and Discovery, offer pet insurance as a product line, but these are lost within such large groups.

Perhaps the best conclusion is that while the pet care industry is a massive growth opportunity, many of the individual investment options in this space have underperformed the broader market.

High valuations, combined with relatively low (or thinning) barriers to entry, have been to blame in many cases (for example Zoetis and Chewy).

That said, this is a durable growth vector and, over time and with reasonable valuations, opportunities are perhaps starting to emerge as major and growing player execute superbly here (for example Colgate-Palmolive and Shoprite).

* Keith McLachlan is CEO of Element Investment Managers.

* McLachlan and/or portfolios managed by him hold shares in Colgate-Palmolive and Sabvest. The latter also has a business relationship with an entity controlled by McLachlan.

This article was republished from Moneyweb. Read the original here.